Overview

Can a consumer data asset be used to support debt?

That was the question facing a private investment firm as it evaluated a proposed $2 million line of credit backed by a commercial consumer database. On paper, the asset appeared to have meaningful value. However, lenders could not rely on internal projections alone. They needed to understand what the data would be worth if the borrower defaulted, the asset had to be transferred, and the market was forced to decide.

Cimply was engaged to conduct an independent data asset valuation and commercial data assessment focused on market value, operational readiness, transferability, governance risk, and downside exposure.

Ultimately, the engagement centered on a simple but uncomfortable question:

What is this data actually worth when the market gets to decide?

Client Context

At the outset, the investor was evaluating a consumer data-driven business whose underlying dataset was positioned internally as a strategic asset and potential component of loan collateral.

As you’d expect, the internal projections assumed meaningful long-term value tied to:

- the size of the database

- niche segmentation of interests and behaviors

- future monetization opportunities

- downstream licensing potential

Specifically, the company believed these characteristics would support long-term value creation.

However, what was missing was an independent assessment of how the data would actually be received by buyers, brokers, lenders, and operators under commercial scrutiny, particularly in downside or time-constrained scenarios.

Importantly, the objective was not to justify a valuation. The objective was to stress-test valuation assumptions against actual market behavior.

The Challenge

Realistically, large datasets often appear valuable in theory. In practice, buyers care about far fewer things than most sellers expect.

In particular, stakeholders needed answers to several critical questions. The lender needed clarity on:

- realistic liquidation value under default or forced-sale conditions

- how the data compared to assets offered by established providers such as Acxiom, Experian, Epsilon, Claritas, Infogroup (now Data Axle), and Stirista

- whether consent language, provenance, and governance controls would survive diligence and transfer scrutiny

- how much value was being lost to structural fragmentation, recency gaps, and operational gaps

- whether the asset could reasonably support premium collateral assumptions

The challenge was not simply measuring size. It was determining whether the data could withstand the kinds of commercial, legal, and operational pressures that emerge when buyers, lenders, and investors begin testing aggressively.

Our Approach

To address these questions, Cimply approached the work to determine the asset’s value, readiness, transferability, and downside exposure the same way an experienced data buyer or lender would:

- assume nothing

- validate aggressively

- test commercial usability

- discount unsupported assumptions quickly

Our thinking focused on realized market conditions rather than theoretical enterprise narratives.

1. Separating the Data from the Business

The first step was intentional separation.

We evaluated the data asset independently from the operating business, excluding future revenue projections, growth assumptions, and narrative positioning from the analysis.

This allowed us to assess what the data could realistically command on its own under distressed, time-sensitive, or liquidation conditions without the benefit of a functioning operating business attached to it.

In practice, that distinction proved critical.

Across the market, standalone data assets are routinely discounted relative to datasets embedded within active revenue-generating ecosystems.

2. Data Readiness and Commercial Viability Assessment

Next, we conducted a structured readiness assessment spanning more than forty operational and commercial evaluation criteria across five domains. As a result, the assessment examined the following areas:

- people and operational capability

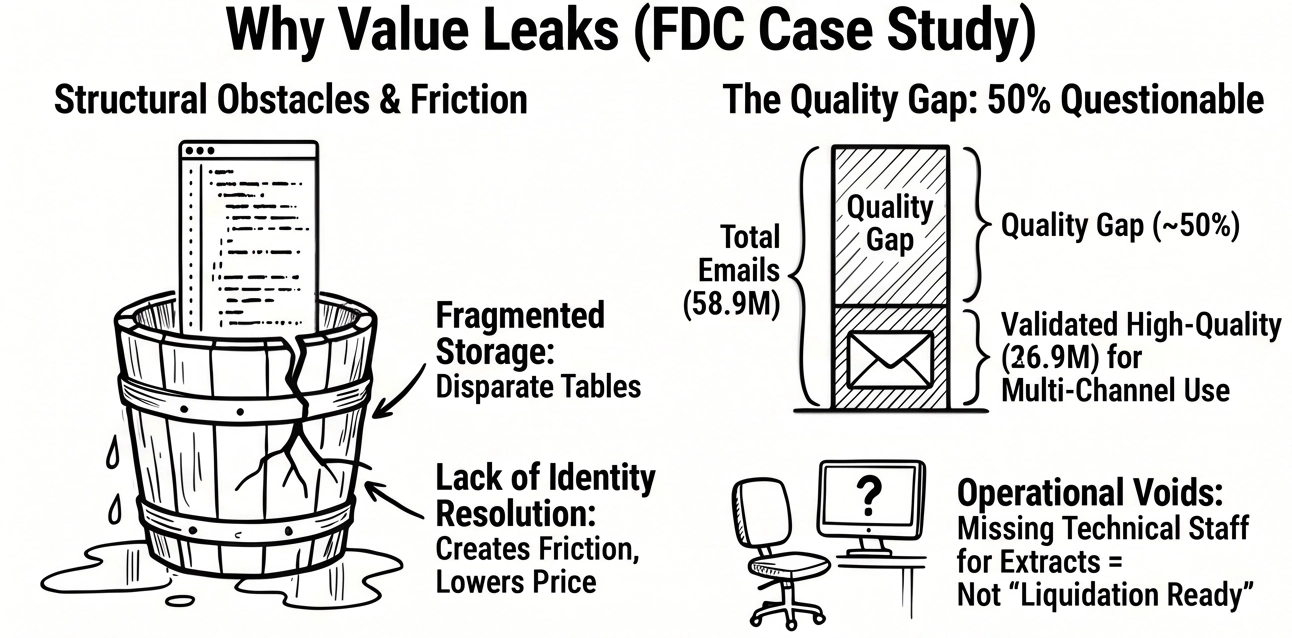

- data structure, linkage, and deduplication

- technology stack and tooling maturity

- governance, consent, and privacy controls

- commercialization and transfer readiness

Not by accident, the assessment focused on the types of issues that routinely reduce buyer confidence, delay transactions, suppress pricing, or eliminate assets from consideration entirely.

Rather than evaluating the data as a pitch deck asset, we evaluated it the way commercial buyers, compilers, and data infrastructure providers evaluate assets in practice.

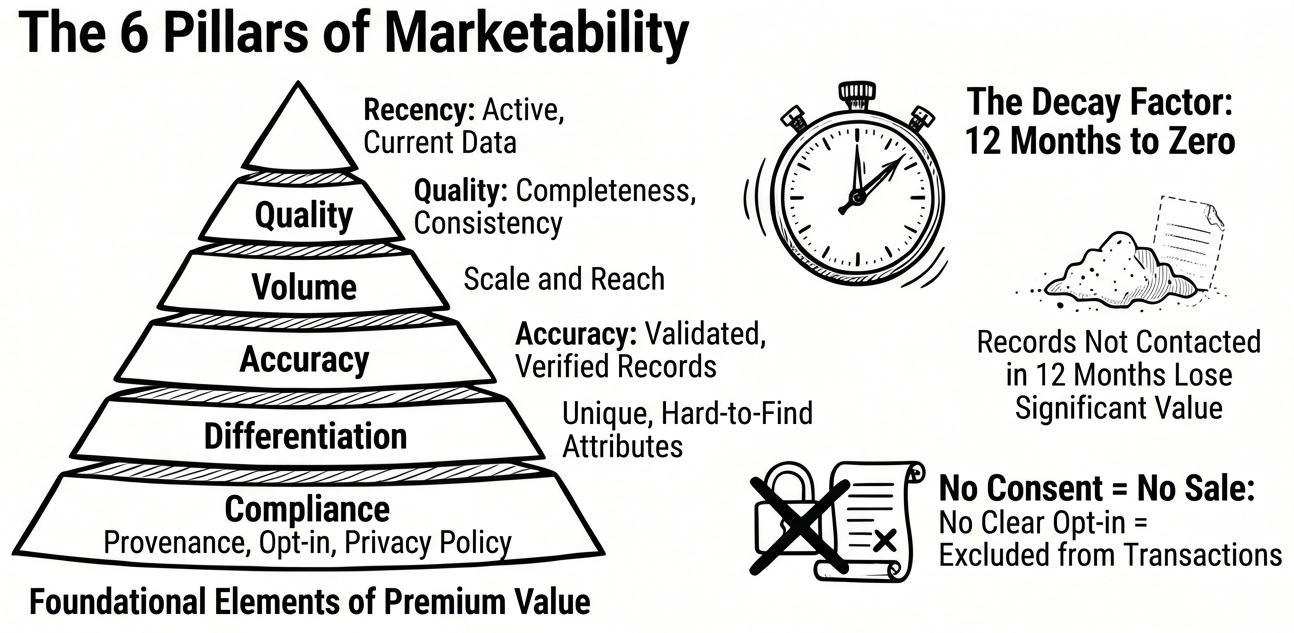

3. Data Quality, Structure, and Recency Analysis

Eventually we reviewed the dataset with specific attention to the factors that significantly influence commercial pricing and transferability. More specifically, we focused on the factors most likely to influence buyer confidence and pricing:

- attribute density and record completeness

- identity resolution and deduplication quality

- channel addressability across email, postal, and digital

- evidence of recency and refresh cadence

- documentation supporting consent and permissible use

- operational readiness for buyer testing and extraction

Where possible, we conducted third-party validation and match analysis against national consumer reference files commonly used by major data compilers and identity providers.

The findings reinforced a common market reality:

Only a fraction of the data drove the majority of the asset’s commercial value.

Several records lacked sufficient validation, recency, or structural integrity to support premium pricing assumptions under buyer scrutiny.

4. Expert Interviews and Buyer Reality Checks

Additionally, to fully ground the analysis in market reality, we conducted fifteen (15) in-depth video interviews with senior executives who had firsthand experience buying, selling, licensing, or liquidating consumer data assets like those we were evaluating.

Cimply assembled the interview participants from our broad network that includes current and former leaders from organizations such as:

| Acxiom | Experian |

| Epsilon | Claritas |

| Infogroup (Data Axle) | Stirista |

| Speedeon | Audience Acuity |

| Identity graph and data infrastructure providers | Other firms involved in distressed asset and bankruptcy transactions |

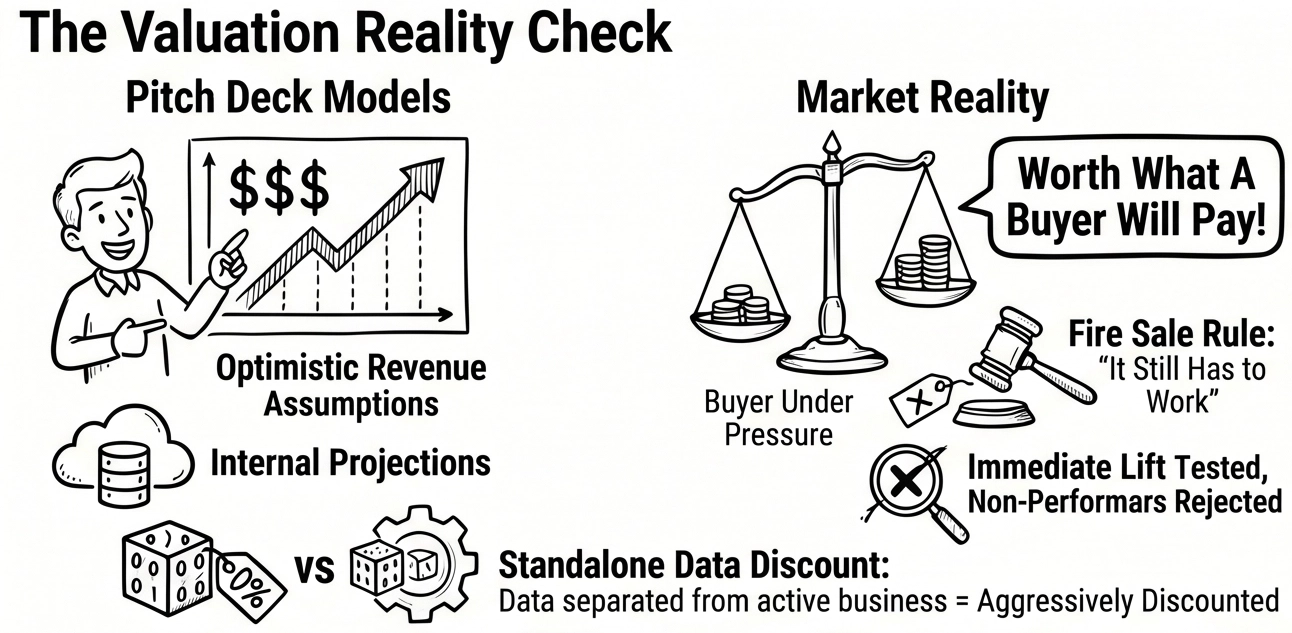

Not suprisingly, several themes surfaced consistently across interviews:

- buyers test aggressively and reject quickly

- published rate cards are irrelevant in liquidation scenarios

- governance and consent gaps significantly reduce buyer appetite

- standalone data assets are routinely discounted relative to active revenue-producing businesses

- operational friction often suppresses realized pricing far more than sellers anticipate

As a matter of fact, one executive summarized it bluntly:

“Even in a fire sale, no one buys data just to buy data. It still has to work.”

5. Market and Pricing Analysis

For comparison, we evaluated the asset against several categories of market participants by conducting a detailed pricing and market comparison analysis across the broad competitive landscape and the comparative benchmarks included:

- national consumer compilers such as Acxiom, Experian, and Epsilon

- wholesale and bulk licensing providers

- identity graph and data co-op providers

- specialty demographic and donor data providers

- retail list providers and commercial data marketplaces

And to ensure all logical scenarios, the pricing analysis evaluated:

- bulk licensing prices by record volume and refresh cadence

- CPM-based valuation ranges under varying quality assumptions

- exclusive versus non-exclusive sale conditions

- historical distressed-sale and liquidation transactions

- realized pricing after suppression, testing, exclusions, and brokerage costs

Lastly, we focused on effective market pricing rather than published list pricing as we know from experience and through the expert interviews, we must make adjustments were made for:

- stale or decaying records

- buyer testing timelines

- operational extraction friction

- governance uncertainty

- brokerage and transaction costs

- commercialization delays

6. Scenario-Based Valuation Modeling

For maximum utility of the assessment, rather than forcing a single valuation number, we modeled multiple market scenarios tied to observable operating conditions.

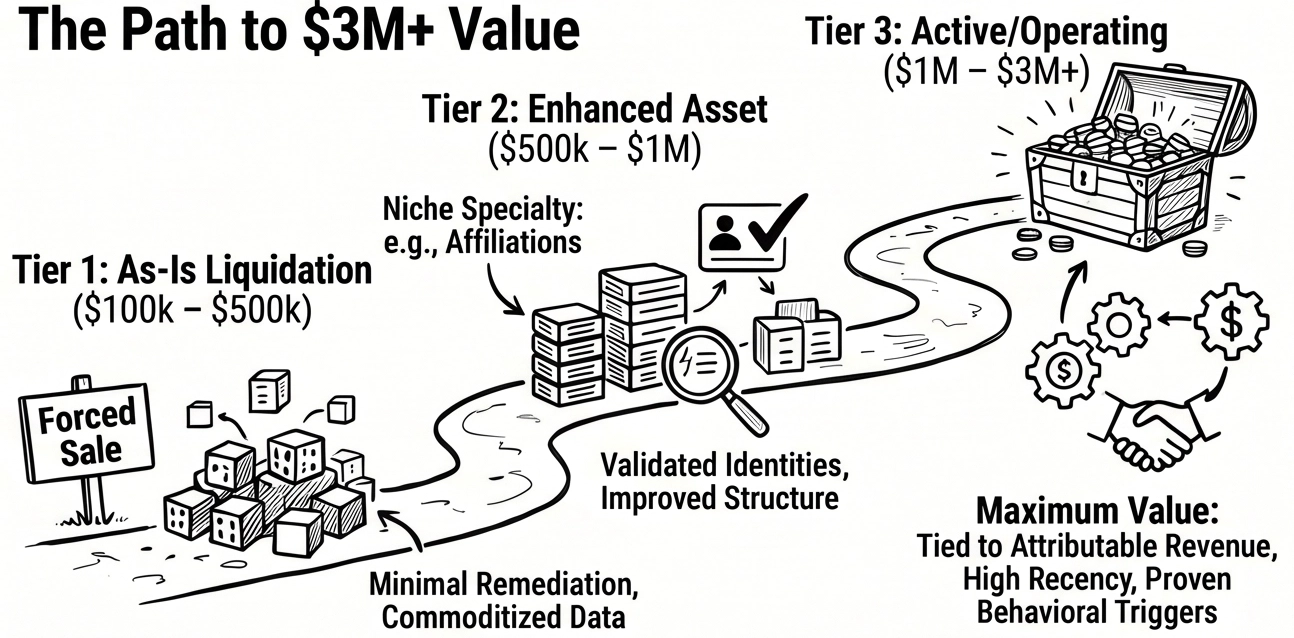

Accordingly, each scenario reflected a different set of business assumptions and these included:

- as-is liquidation value under forced-sale assumptions

- enhanced but inactive value assuming remediation and structural improvements

- operating value where the data actively supported measurable revenue generation

As a result, the modeling provided stakeholders with a clearer understanding of:

- where value leakage existed

- what remediation would be required to improve value

- how operational maturity impacted transferability and pricing

- how significantly different liquidation value could become from projected enterprise value narratives

Key Findings

By the end of the assessment, several conclusions became unavoidable:

- in its current state, the dataset did not support premium valuation assumptions relative to established commercial data providers

- under liquidation conditions, buyers would likely acquire only the cleanest and most commercially viable subsets while discounting aggressively

- governance ambiguity and consent limitations significantly constrained ability to transfer

- portions of the asset lacked the recency, structure, and operational readiness required to support lender-grade collateral assumptions

- realized market value differed substantially from internally projected valuation expectations

Across interviews, benchmarks, and buyer-side discussions, one point remained consistent:

Data becomes much more valuable when it is tied to ongoing revenue generation and observable customer behavior.

Deliverables

We delivered a confidential, lender-ready Data Asset Valuation and Liquidation Readiness Report that incorporated several supporting analyses and recommendations that included:

- valuation drivers and inhibitors

- commercial readiness findings

- comparable provider and transaction benchmarks

- buyer-side expert commentary

- scenario-based valuation modeling

- governance and operational risk observations

- remediation opportunities tied to future value improvement

The report was designed to withstand scrutiny from lenders, investors, legal counsel, and commercial operators evaluating downside exposure and collateral risk.

Outcome

The engagement ultimately provided the lender with a totally different view of the underlying risk associated with the proposed financing structure.

The operating company was seeking a $2 million line of credit backed in part by the perceived value of the underlying consumer data asset. While internal projections and narrative positioning suggested substantial long-term value, the independent assessment revealed significant gaps between modeled assumptions and likely market behavior under real-world liquidation conditions.

Our analysis demonstrated that:

- only a subset of the data would likely retain meaningful commercial value under buyer scrutiny

- governance and consent limitations significantly constrained transferability

- portions of the asset lacked the structure, recency, and operational readiness required to support premium valuation assumptions

- liquidation pricing expectations differed substantially from projected enterprise value narratives

As a result, the lender elected not to proceed with the requested financing structure.

The engagement helped the client:

- avoid a potentially high-risk lending position tied to overstated collateral assumptions

- replace speculative valuation narratives with market-based evidence

- establish a more defensible view of downside exposure

- align investment, legal, and operating stakeholders around realistic commercial conditions

Most importantly, the work reframed the discussion from theoretical asset value to practical market liquidity, transferability, and buyer behavior under pressure.

Why This Matters

This engagement reflects how we approach data valuation and commercialization: without exaggeration, without inflated assumptions, and without confusing scale with marketability.

Large datasets can appear valuable on paper. In practice, buyers, lenders, and investors evaluate data the same way markets evaluate any other commercial asset: through usability, transferability, governance, recency, and the ability to generate measurable economic value.

Data does not become valuable simply because it exists. It becomes valuable when it is operationally sound, commercially usable, legally defensible, and capable of producing real business outcomes.

Our role is to help clients understand the difference before the market forces them to.